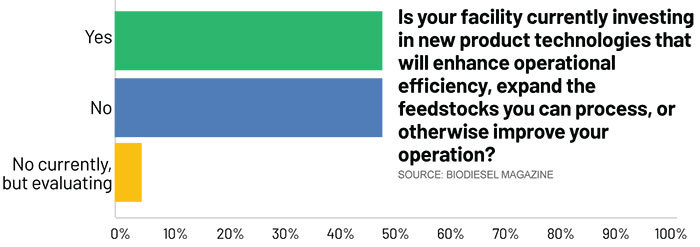

Holding Strong: U.S. Biodiesel Producers Surveyed

January 13, 2021

BY Tom Bryan

Advertisement

Advertisement

Related Stories

Now in its seventh year since the B20 requirements were enacted, the state of Minnesota is beginning its transition toward a 20-percent biodiesel blend (B20) during the summer months.

Neste and Air New Zealand have signed an agreement for the supply of 2.4 million gallons of neat Neste MY Sustainable Aviation Fuel. The agreement follows an earlier SAF delivery to Air New Zealand in 2022.

Desert Jet has partnered with TITAN Aviation Fuels to establish the supply of sustainable aviation fuel (SAF) at its flagship FBO, Desert Jet Center at KTRM, including using SAF for its charter aircraft fleet.

The USDA maintained its forecast for 2023-’24 soybean oil use in biofuel production in its latest World Agricultural Supply and Demand Estimates report, released April 11. The forecasted price for soybean oil was also unchanged.

The U.S. Department of Energy will award up $18.8 million to address research and development (R&D) challenges in converting algae, such as seaweeds and other wet waste feedstocks, to biofuels and bioproducts.

Upcoming Events

@ Copyright 2024 - BBI International - All rights reserved.